Terms and conditions update: From 24 August, we're updating our Savings Account and Payment Services T&Cs, including transaction and payment limits. Learn more.

Terms and conditions update: From 24 August, we're updating our Savings Account and Payment Services T&Cs, including transaction and payment limits. Learn more.

To find out your borrowing power simply, fill out this form and a Qudos Bank representative will reach out with more information.

To apply for a home loan with us, you can get in contact with our friendly team to process your application via telephone, online or in person at one of our branches. If you’re looking for a step-by-step guide on how to apply for a home loan, then check out our Home Loan Application Checklist and Guide to help you through the process. You can also check out our Home Loan Application Process Page for more information on the home loan process

Offset accounts work as a transaction account linked to your home loan. The money in that account 'offsets' daily against the balance of your loan. So, it reduces the interest you need to pay because interest is only charged on your net balance (i.e. your overall loan balance minus your offset account balance). In other words, the loan 'thinks' you've paid that money off your loan already, reducing the interest charged accordingly. Qudos Bank offers multiple offset accounts on most home loans, check with your lending specialist.

A split rate home loan, also known as a split mortgage, allows you to divide your home loan into multiple accounts, each of which has different interest rates and features. The most common way to set this up is to have a portion of the loan at a fixed interest rate, while the remainder has a variable interest rate. Read more about split home loans in our blog.

Qudos does not impose a maximum limit, however there are minimum loan amounts that may apply.

Redraw is a simple way to access additional repayments that you have made on your home loan above the minimum required repayments, to pay for renovations or other expenses.

Once you have your home loan, you are required to make minimum repayments. If you make additional repayments above what is required and redraw is available on your home loan, these additional funds become part of your available redraw.

^Provided the customer was not in arrears at the start of the period and that all required payments are made in accordance with the loan contract.

Any money in your redraw reduces the balance owing on your home loan. This means that you'll be paying less interest on your home loan.

Redraw can be helpful if you want to use the money at a later date - for home renovations, pay off debts like credit cards or personal loans, or to make purchases you may otherwise use a personal loan for, like a car or holiday.

1. Login in to your Online Banking account.

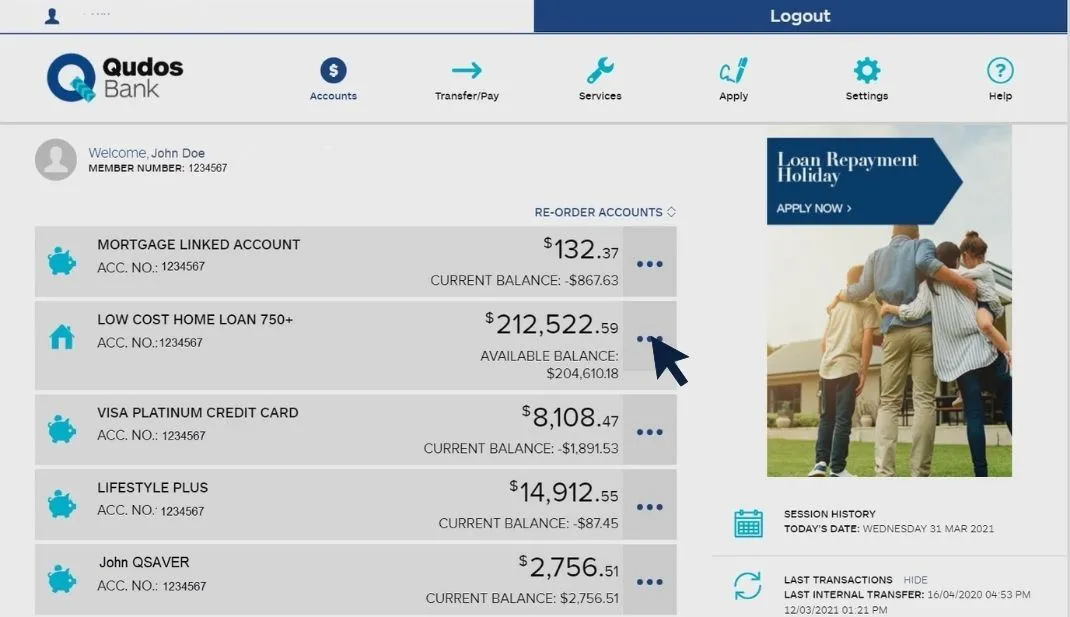

2. Click the three dots next to the home loan account you want to redraw from. The available balance amount is your available redraw.

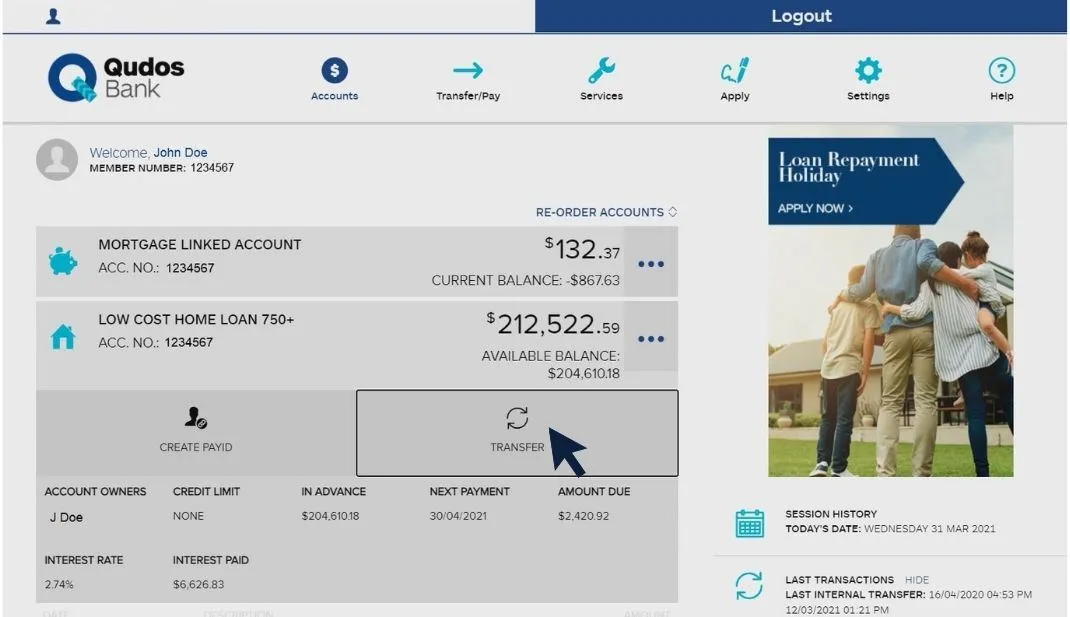

3. Select 'Transfer'.

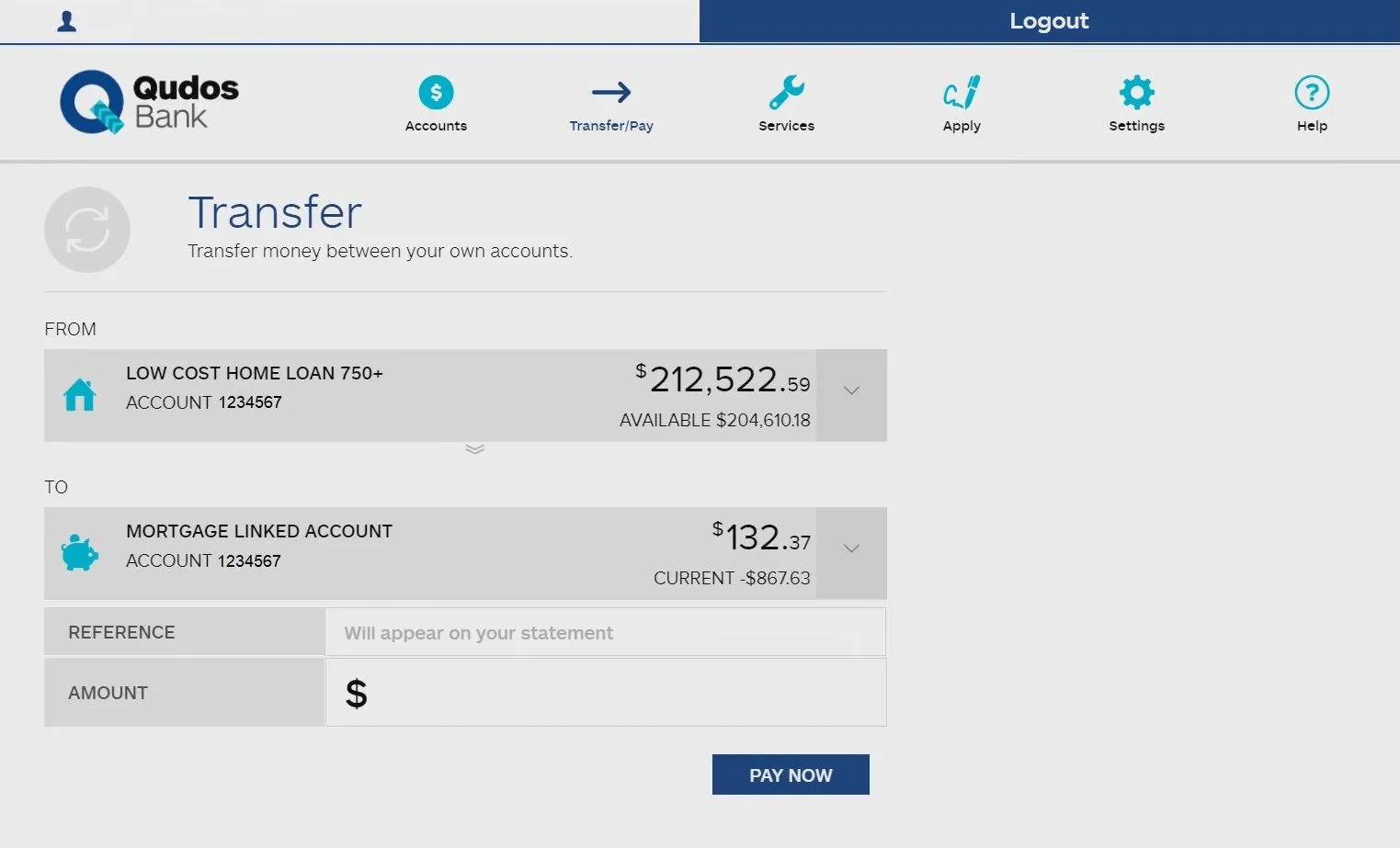

4. Then follow the prompts to transfer fund into your preferred savings account.*

*Redraw terms and conditions apply and redraw is only available for certain home loans. Redraw is subject to our approval. We may change, suspendor terminate the redraw facility at any time.

A comparison rate is the interest rate plus most fees and charges relating to a loan. The comparison rate helps you work out the true cost of a loan and makes it easier for you to compare similar loans and rates from different lenders.

Most Qudos Bank Home Loans offer two repayments types, these are:

The difference between the two is that principal and interest repayments mean you will be paying down your principal balance (as well as interest it accrues) from your first repayment. Whereas, with interest-only repayments, the principal balance will not be reduced and interest continues to be calculated during this period.

*Interest only subject to approval. During an interest only period, your interest only payments will not reduce your loan balance. This may mean you pay more interest over the life of the loan.

The interest-only term will depend on your circumstances. 5 years is the maximum we will allow; after which the interest rate will revert to the applicable variable principal and interest rate.

Lenders Mortgage Insurance (LMI) protects the lender if you default on your home loan. In these circumstances, the lender may need to sell your property to recover the cost. Should the sale of your home not cover the outstanding amount owing to your lender, this is known as a 'shortfall'. LMI is not designed to protect you as the borrower, but rather its purpose is to protect lenders in case of a shortfall, and allows the lender to lend the borrower an amount higher than the lender would otherwise be able to provide. A typical scenario is being able to borrow more than 80% for a standard metro residential property (subject to approval).

Lenders Mortgage Insurance (LMI) is deducted from your loan proceeds. To assist borrowers Qudos Bank, in some cases, may allow you to add the premium to your loan amount and repay it with your home loan repayments.

Once you've decided to take up the fixed rate lock in feature, simply complete and sign our Lock In Request form. Once completed, e-mail it to your Lending Specialist who will arrange to lock in the rate for you. Alternatively our branch or contact centre teams can provide this form at any time during the application process.

If you have an existing fixed rate home loan that is about to end or you wish to switch to a fixed rate loan, you can also lock in the rate. Give us a call to discuss your rate lock options.

A fixed rate home loan locks in the interest rate and repayments for a fixed period, usually between 1 to 5 years.

Potentially yes. Prior to the expiry of your loan we will write to you to get in contact with us to discuss your options.

No, unfortunately offset accounts are not available on fixed rate loans. However, we offer 100% multiple offset accounts on many of our other competitive home loans.

A rate lock for a fixed rate home loan enables fixed rate home loan applicants to hold the current fixed rate for their chosen term for a 90 day period starting from when the application is applied.

The fee associated with a rate lock is 0.10% of approved loan amount (minimum fee $50), and this fee must be paid up front. The rate will be locked in once the form is received and the fee is paid in full. If you are switching from another product to a fixed rate loan and require rate lock, the fee will be deducted from your nominated Qudos account or you can pay by credit/debit cards. For new loans, If the loan is not funded prior to the rate lock expiry, the rate lock fee is still payable. If the fixed rate changes within the 90 day period, the rate lock will guarantee you the lower of the current rate or rate locked in at the time the rate lock application is applied. Please call us for more information or to apply for a rate lock please complete the rate lock form.

The fixed rate which is current on the day of lock in, is the rate which is guaranteed for a period of 90 days from the time the rate lock fee is paid.

Yes, if the 90 days fixed rate lock period has expired and you're interested in locking for a further 90 days, you will need to pay a further fee. The applicable fixed rate will be the rate locked in at the time the second fee is paid.

The rate can be locked at any time until settlement. However, if your contract has been issued it will need to be re-issued.

At settlement, if the usual fixed rate is lower than the locked in rate, you'll receive the lower rate. For example, a rate locked at 3.99% on the 5 October, settlement occurs 12 November and the usual rate on the 12th is 3.69%, you'll receive the 3.69%.

No, the fixed rate lock fee must be paid up front. The fixed rate will be locked in once the Lock In Request form is received and the fee is paid in full.

The rate lock fee will only be refunded if the application is declined. No refunds apply if you choose not to proceed with your application.

Unlike a fixed-rate home loan which locks in a certain interest rate, a variable home loan is a home loan on which the interest can vary and fluctuate up and down.

Yes, we offer the option for you to divide your home loan into multiple accounts across different variable rate products so you can access the different loan features in the way that suits you.

A package home loan is a home loan that combines your home loan with a host of other products and features into one bundle. A package home loan offers extra benefits such as a Personal Loan application fee waiver and a Platinum credit card annual fee waiver.

A construction loan allows you to build or renovate and pay the builder when key stages of the build are complete.

Unlike home loans, which you typically receive the whole loan amount at settlement, construction loans allows funds to be drawn in stages, as you receive progress payment requests from your builder and tradespeople.

Builders will often require a deposit before plans are drawn up and/or building work commences. Please speak to your builder as these requirements vary from builder to builder.

The loan will allow up to 12 months to complete construction.

Yes, Qudos Bank's home loans feature a discharge fee of up to $275.

Yes. A fixed lock fee is payable for each fixed rate home loan split, if you wish to lock in the rate on each split.

Unlike a fixed-rate home loan which locks in a certain interest rate, a variable home loan is a home loan on which the interest can vary and fluctuate up and down.

Yes, we offer the option for you to divide your home loan into multiple accounts across different variable rate products so you can access the different loan features in the way that suits you.

A package home loan is a home loan that combines your home loan with a host of other products and features into one bundle. A package home loan offers extra benefits such as a Personal Loan application fee waiver and a Platinum credit card annual fee waiver.

Yes. You can switch from a variable rate loan to a fixed rate loan at any time so long as the loan amount and structure of your loan does not change.

All loans can be paid out at any time. Variable rate loans can be done so by paying out the discharge balance. Fixed rate loans may attract break costs if you are paying the loan out within the fixed rate period.

Depending on the home loan selected repayments can be made monthly, fortnightly or weekly. Interest-only repayments must be made monthly. The ability to make additional payments will also be dependant on the type of loan you have. Loans that have variable rates can have additional payments made at any time. For loans with Fixed rates, you can pay up to $10,000 per year without incurring break costs.

You can access the repayment you have made over and above your regular required repayments at any time by Online Banking or the Mobile app.

[Fixed Rate Loans] Yes, you can make additional repayments on your fixed-rate home loan of up to $10,000 a year without incurring break costs. For payments, greater than $10,000 per year break costs may be payable.

[Variable Rate Loans] Yes, you can make unlimited additional repayments on Qudos Bank's variable interest home loans.Use our Extra Repayments Calculator to help you better manage your loan.

Repaying a fixed rate loan early may result in incurring break costs. Please call us so we can discuss your options with you.

Qudos Bank offers unlimited multiple offset accounts on applicable loans.

No, there is no minimum redraw amount for redraw transactions completed via Online Banking or the Mobile App.

Our loan interest calculation method allows for up to ten decimal places in rounding the daily interest rate.

Example 1:

*Assuming the daily balance outstanding is $500,000 over a 31 day month

Example 2

*Assuming the daily balance outstanding is $500,000 over a 31 day month

In some cases, we may agree to extend your interest only term when your loan nears the interest only expiry date. This will depend on your circumstances and will be subject to assessment.

No. All applications for additional funds are assessed and are subject to lending criteria, and associated terms and conditions.

We respectfully acknowledge the Traditional Custodians of all the lands on which we live and work, and we pay our respects to Elders past and present. We recognise their continued connection to the land, waters and culture and we acknowledge that sovereignty has never been ceded. Our head offices are located on the land of the Wurundjeri Woi Wurrung people of the Kulin Nation in Victoria, and the land of the Gadigal people of the Eora Nation in New South Wales.

We are an equal opportunity employer that celebrates the diversity, equity and inclusion of all people.

.svg)